A story from one of my own clients — a cancer warrior.

I’m sharing this to highlight my personal experience in handling a declined Guarantee Letter (GL) for a client who was undergoing cancer treatment.

Dia disahkan breast cancer in 2021.

Certificate belum pun cukup 24 bulan masa tu. Still dalam contestable period.

Diagnosed kat hospital private A. Tapi annual limit medical card dia cuma RM150K je. So saya nasihatkan dia teruskan rawatan kat Government Hospital.

To receive treatment at a private hospital, you’ll either need sufficient funds or a comprehensive medical coverage plan.

Yelah… kalau accident pun ada my client bill sampai RM300K setahun, ini pula cancer.

Tapi ramai tak tahu, rawatan kat GH pun bukan semua free/subsidized. Ada ubat yang kena beli sendiri. Masa tu cancer baru kena sebelah breast. Cost ubat cancer sahaja dah RM5,000 sebulan. Dia kena bayar sendiri dulu, baru submit claim kat AIA.

Government hospitals provide great care, but not everything is fully subsidised.

Some medications and treatments are not covered at all.

Disebabkan cert tu belum 2 tahun, claim terus kena investigation.

Gambar sekadar hiasan.

Some medical investigations may require reports from clinics near your workplace or home. The cost will be reimbursed by the takaful operator directly into the client’s bank account.

Mula-mula, kena minta doctors isi Attending Physician Statement (APS) and minta report dari Government Hospital dan beberapa klinik sekitar rumah dan tempat kerja. Lepas beberapa lama (lagi-lagi time MCO, memang lama gila), dapat report dari Government Hospital — tapi dalam tu mention pernah pergi Hospital Private A. So next, kena minta report dari Hospital Private A.

Bila dah dapat, rupanya dalam report and APS tu mention Hospital Private B pula. So kena request APS and report dari Hospital Private B.

Not the actual Attending Physician Statement or Medical Report.

Bila dapat, laaaa tak lengkap pula! Kena reapply. Tunggu lagi…

Bayangkan, semua ni ambil masa hampir setahun. Semua orang stress. Client saya yang tengah sakit lagi la… mentally & emotionally drained.

Tapi Alhamdulillah, akhirnya berjaya buktikan tiada pre-existing illnesses. Rasa nak sujud syukur, nak cium tanah bila claim finally lulus.

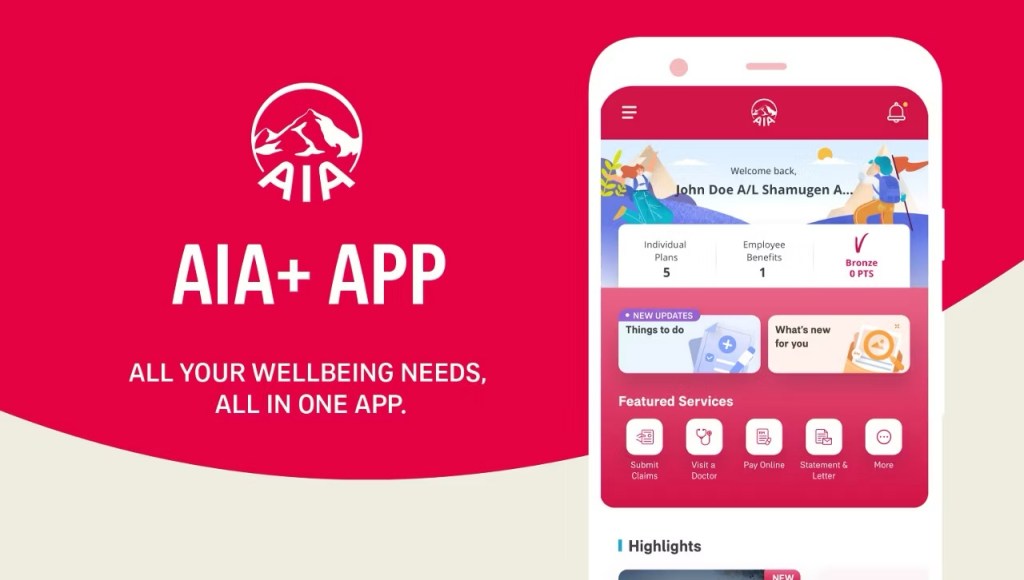

Lepas tu claim memang smooth. Submit kat AIA+ app je.

You can now use the AIA+ app for many things—like changing your payment method or frequency, submitting claims, checking your GL status, and monitoring all your AIA plans in one place.

Tapi… cancer tu dah merebak ke breast lagi satu. Bukan tu je — dah metastasized ke organ lain juga.

Cost ubat cancer dah cecah lebih RM10,000 sebulan, belum campur ubat lain lagi. Semua dia bayar dulu, baru claim.

Sampai ke akhir hayat, dia teruskan rawatan dengan duit sendiri dulu — nasib baik dia mampu bayar dulu, baru claim balik.

Saya tak boleh reveal nama dia. Tapi siapa yang baca ni, tolong sedekahkan Al-Fatihah dan doakan kesejahteraan arwah.

Content creator & Islamic financial planner who keeps things fun, relatable & practical. Juggling life, family & great deals—always with a smile!

And hey, if you ever want to chat about retirement savings or financial planning, just hit me up! Let’s chat! ☎️ 012 223 1623[WhatsApp link]

I’m so glad you enjoy my articles, photos, and videos! Let’s keep it respectful—please don’t copy, reproduce, or share them without my permission. If you’d like to use something, just send me a quick message. I’d be happy to chat!

Rumah Untuk Alie

If I were Gianla, Alie’s mom, this movie would have turned into a horror genre instead of a melodrama. Because I would have crawled out from my grave to haunt—and teach a lesson to—those who bullied my daughter.

Full On Kenduri Mode at APTB Raya Open House

If there’s one thing AiA Public Takaful knows how to do, it’s throw a proper jamuan!

This year’s Raya Open House was basically a full-on kenduri — we’re talking rendang, soto, satey, kambing golek, and to top it off, bottomless Tealive drinks and Inside Scoop ice cream. Lupakan je la nak diet, kita start esok je ok!

WHEN THE PAYCHECK STOPS BUT THE BILLS DON’T

Money. You don’t think about it much—until you don’t have enough of it.

Imagine this: One day, life is normal. You’re working, paying bills, maybe even saving a little. Then, out of nowhere, you get hit with the kind of news that stops time—cancer, a heart attack, stroke, something big. Suddenly, work is no longer an option. Not because you don’t want to, but because your body says, “No, not today. Not ever, maybe.”

Leave a comment