Part 1 of 3 — What Actually Happens Before Your Initial GL Gets Approved

Many people think hospital admission starts when the medical card is presented.

In reality, there’s usually a process happening between the doctor, hospital, and insurer before an Initial GL is approved.

This series walks through that journey step by step — and in Part 1, we start with the first stage: Initial GL.

- Initial GL

- What is an Initial GL?

- Why might the Initial GL not be enough?

- What is a Final GL?

- Why can Final GL take time?

- Common Misunderstandings

- Putting It All Together

- What Comes Next

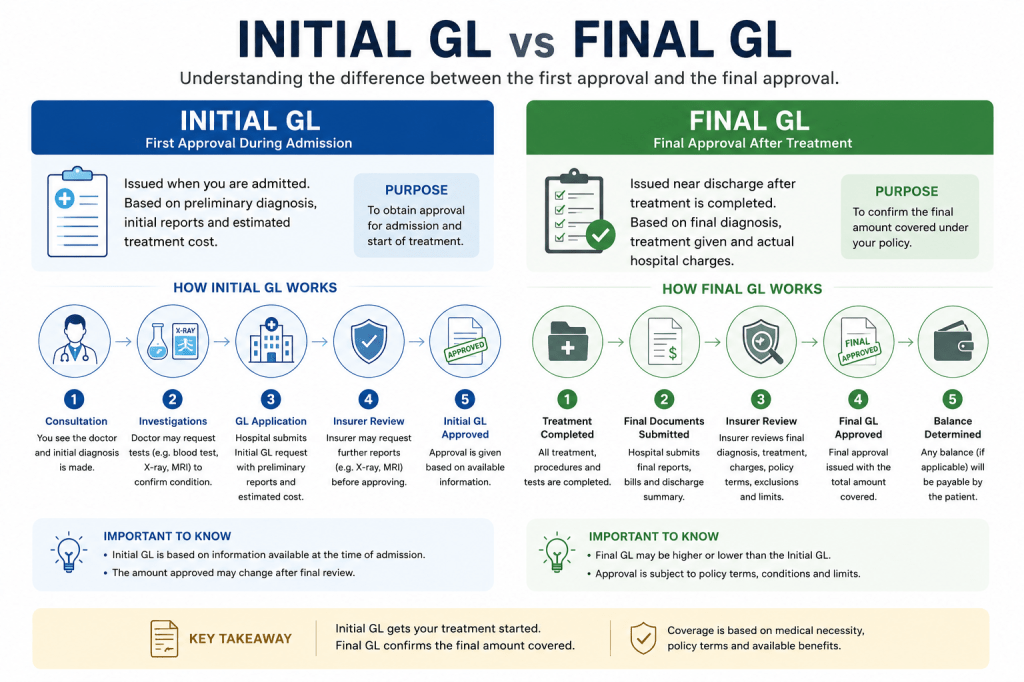

Initial GL

If you’ve ever been admitted to a hospital and heard terms like “Initial GL approved” or “waiting for Final GL”, it can sound more complicated than it actually is.

A Guarantee Letter (GL) is essentially a payment commitment issued by an insurer, employer, or medical administrator to the hospital. It confirms that eligible medical costs will be covered based on your policy or benefits.

Think of it as authorization to proceed with treatment under your coverage — not a blank cheque for every possible charge.

What is an Initial GL?

An Initial Guarantee Letter is the first approval issued when you are admitted.

At this stage, the insurer only has limited information:

- Your symptoms

- Doctor’s preliminary diagnosis

- Estimated treatment plan

- Estimated admission cost

Because of that, the insurer approves an initial amount based on what is known at that moment.

Example:

You are admitted for severe abdominal pain.

The hospital estimates treatment may cost RM8,000.

The insurer issues an Initial GL for RM8,000 so admission and treatment can begin.

Important:

The Initial GL is not the final approved amount. It is more like a starting authorization.

Why might the Initial GL not be enough?

Medical treatment evolves.

During admission:

- More tests may be required

- Diagnosis may change

- Surgery may become necessary

- Hospital stay may extend

When this happens, the hospital submits updated medical information and revised costs to request additional approval.

This leads to the Final GL.

What is a Final GL?

The Final Guarantee Letter is issued near discharge once treatment is completed and actual charges are clearer.

At this stage, the insurer reviews:

- Final diagnosis

- Treatment received

- Hospital charges

- Policy eligibility

- Exclusions and limits

Example:

Initial GL: RM8,000

Actual treatment cost after surgery and extended stay: RM15,000

Hospital submits documents → insurer reviews → Final GL approved for RM15,000 (subject to policy terms).

This final approval determines how much is covered and whether any balance remains payable by the patient.

Why can Final GL take time?

Final GL approval often takes longer because more checks are involved:

- Verification of diagnosis

- Review of medical reports

- Policy coverage checks

- Assessment of exclusions or waiting periods

- Confirmation of final billing

This is why discharge can sometimes be delayed even after the doctor says you’re medically fit to go home.

Common Misunderstandings

“My Initial GL was approved, so everything is covered.”

Not necessarily. Final coverage depends on actual treatment and policy terms.

“Final GL means the insurer is delaying payment.”

Not always. Hospitals and insurers usually need complete documentation before final approval.

“If my bill exceeds the Initial GL, I must pay immediately.”

Not necessarily. Hospitals often request an additional GL first before asking for payment.

Putting It All Together

Initial GL gets treatment moving.

Final GL closes the case and confirms what is ultimately covered.

Understanding the difference helps reduce surprises during admission and discharge — and makes it easier to know what questions to ask your hospital and insurer.

What Comes Next

Initial GL is only the beginning of the process.

In Part 2, we’ll look at what happens after admission: how hospitals request additional GL, why approved amounts can change, and what actually happens before Final GL is issued.

Read Part 2 : How Initial Guarantee Letter (GL) Actually Works: From Seeing the Doctor to Getting Hospital Admission Approved

Read Part 3 : Does a RM1 Million Annual Limit Mean You Automatically Get RM1 Million?

Disclaimer: This article is shared for general information and educational purposes only and does not represent any insurance company, takaful operator, hospital, or third-party administrator. Actual GL processes, coverage decisions, and claim outcomes may differ depending on policy terms, medical findings, and individual circumstances.

Leave a comment